TCIB (Transactions Cleared on an Immediate Basis) is an initiative in the SADC (Southern African Development Community) region that aims to increase financial inclusion by providing a system for low-value real-time cross-border interbank payments. As a bank, here's what you should consider when deciding where such a programme could fit into your technology space.

The TCIB initiative is bound to be good news for consumers as it promises to provide greater choice, reduce dependency on cash, and increase the speed of small transfers of money within the region. But before these benefits can be realised by consumers, banks need to implement a system that allows them to participate in the network. As a bank, how do you do this and where does such a system fit into your existing infrastructure?

A simple way to think about it is in the same way you would a card issuing and acquiring platform. In order to offer customers the means to make or receive payments via the major card schemes, you need the technology by which you can connect your core banking system to the card payment rails.

The low-value international remittance space is analogous to card issuing and acquiring in a number of ways. In the context of remittances, ‘acquiring’ can be defined as the mechanism by which a bank receives deposits from a money transfer scheme. Similarly, ‘issuing’ can be defined as giving customers the ability to initiate immediate and cheap international transfers to any recipient from the comfort of their banking app. Instead of a card scheme, the backbone of the interbank payment network would be a remittance scheme, such as TCIB, but could also include services provided by other money transfer operators.

From an infrastructure perspective, we could thus imagine a remittance issuing and acquiring platform living alongside a bank’s card, core banking, forex, and back-office systems.

Tooling for cross-border remittances: Factors you need to consider

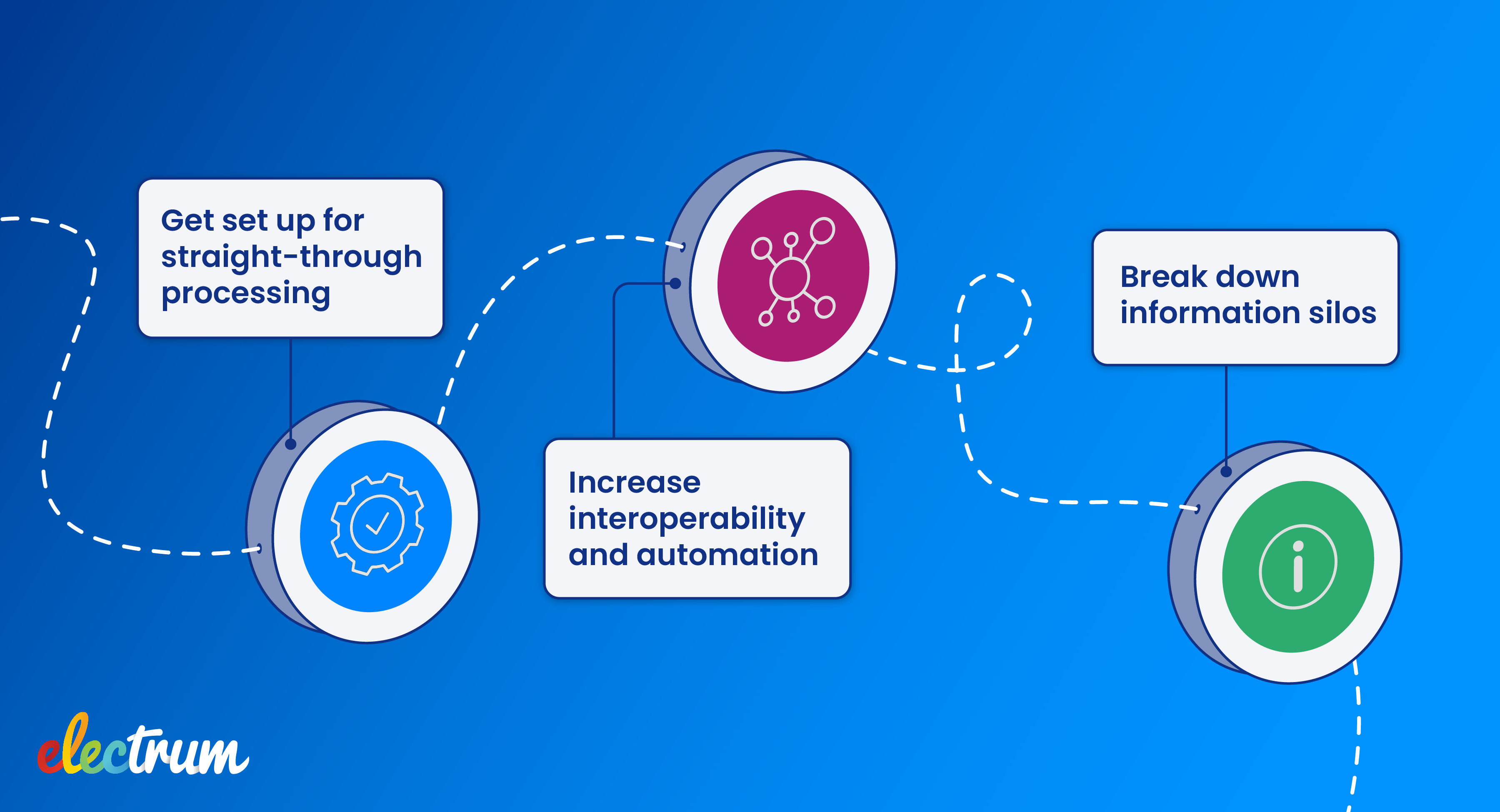

Given that the card payment space is highly mature – and a card platform is such an essential part of the bank’s infrastructure – you would typically choose a ready-made issuing and acquiring platform from a trusted vendor who specialises in such technology. But, since the low-value remittance space has nowhere near the same level of maturity in terms of interface protocols, interoperability standards, and regulation, it might not be so obvious what features and functionality such a platform will need to provide.

Here’s what we think you should consider when thinking about what a low-value cross-border remittance platform would look like for you:

Integration into the network

At the very least, the platform will need to connect into the remittance scheme. In the case of TCIB, the protocol used is a subset of the ISO20022 messaging standard. Other money transfer operators typically use proprietary APIs, which leads to the next point:

Flexibility and extensibility

A fundamental benefit of the TCIB initiative is that it enables cross-border interoperability between banks, with centralised clearing and regulation. So any bank connecting into it will be part of an interoperable network. But to reach further into the broader network of money transfer operators, and to keep up with a rapidly changing segment of the industry, a remittance platform will need to be adaptable. The ability to accommodate new products and services – and changes to existing ones – will be key to providing customers with the most comprehensive offering.

Compatibility with legacy systems

The established components of a bank’s technology have usually been around a long time and will likely not be going anywhere in the near future. Any new technology brought into this space will need to be introduced without disrupting operations, and without adding burdensome processes. If there is a strategy to replace legacy platforms, then the remittance component must complement the move to newer technologies.

Sending, receiving, or both?

The receiving leg of a money transfer is the less complicated of the two: landing the payment from the network, crediting the recipient’s account, and recording the transaction for reconciliation and settlement. Sending, on the other hand, requires channel integration to receive incoming payment instructions, management of the payment request state (i.e. the order lifecycle of a money transfer), as well as communicating externally with the payment network and internally with banking systems. It would be logical for a bank to support both sending and receiving, but there are cases where one could be prioritised over the other. For example, a bank in a country that has a high net inflow of remittances from abroad might first only support receiving, and perhaps later add sending, should there prove to be a viable business case for the latter.

Operational troubleshooting

Tools that provide a view on operational processes and allow for rapid resolution of issues are essential for a good customer experience.

Settlement and reconciliation

Automatic and real-time generation of the artefacts required to initiate settlement and to reconcile transaction records will reduce reliance on manual processes, as well as help manage liquidity risk by having a constantly updated view of settlement obligations.

Compliance and reporting

Adherence to industry security standards and providing the necessary reporting to regulators are of course non-negotiable. Fraud mitigation, anti money laundering and KYC (know your customer) measures are also must-haves.

Business insight

Finally, perhaps the most overlooked features of any transaction processing software are those that contribute to tracking business metrics. Data and reports that are easily accessible and can feed into business intelligence tools are a great value-add.

To sum-up, for you to participate in an initiative like TCIB, it would make sense to consider your choice of technology as not just an ad-hoc solution, but rather a comprehensive and integrated component of your banking infrastructure. Just like card issuing and acquiring, but for low-value cross-border remittances.

If you’d like to find out more about how Electrum can help get you started with this exciting initiative, reach out to us here.